Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

Earlier in the spring, the Federal Housing Administration (FHA) announced that, starting in late May 2025, H-1B visa holders and other non-permanent residents would be banned from taking out new FHA mortgages.

The result?

Non-permanent residents—including H-1B visa holders—saw their share of FHA mortgage locks crater from 3.8% in September 2024 to 0.2% in September 2025, according to Optimal Blue. This sharp pullback comes after their share of FHA mortgage locks had spiked between 2020 and 2024.

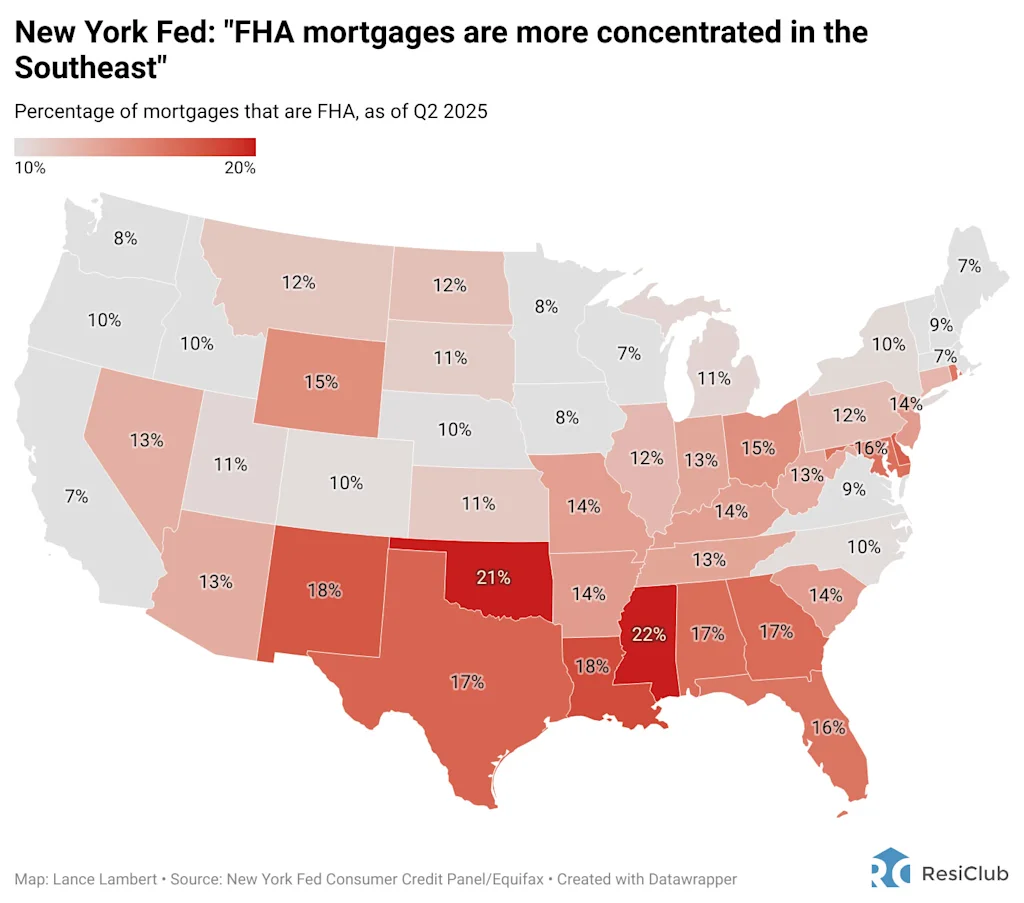

Keep in mind that FHA mortgages make up a much smaller share of overall borrowers than, say, GSE conventional borrowers. Indeed, Optimal Blue data reviewed by ResiClub shows that FHA mortgages accounted for 22.0% of total U.S. mortgage-purchase locks in September 2025. Meanwhile, according to the New York Fed, as of June 2025, FHA mortgages represent just 12% of the nation’s $12.94 trillion in mortgage debt.

While FHA has pulled back on lending to H-1B visa holders, as far as ResiClub can tell there hasn’t been a similar change—at least not yet—in the conventional mortgage space (Fannie Mae/Freddie Mac).

“This squeezes entry-level homebuying in some key housing markets already dealing with weak sales and too much supply,” writes Eric Finnigan, president of Demographics Research at John Burns Research and Consulting. (JBREC published a report in October on the topic for its clients.)

As an example of a potentially affected housing market, Finnigan points to Fayetteville, AR—which is where Walmart is headquartered. Walmart HQ has reportedly paused new H-1B hiring in late 2025 after the Trump administration announced it’d impose a $100,000 fee for certain new H-1B applications.

“Walmart HQ stops new H-1B hiring due to $100K fee. Lines up with research we sent to clients last week calling out Walmart HQ’s metro [Fayetteville] as 1 of ~15 local housing markets most exposed to H-1B changes, based on analysis of loan-level data by citizenship status,” wrote Finnigan in October.

While growth markets in the South—particularly those with the higher levels of homebuilding, such as Dallas, TX; Fayetteville, AR; and Durham, NC—might feel a sharper housing-demand contraction from this specific FHA policy change, they aren’t necessarily the markets that would see the greatest softening if there were a broader pullback in H-1B activity.

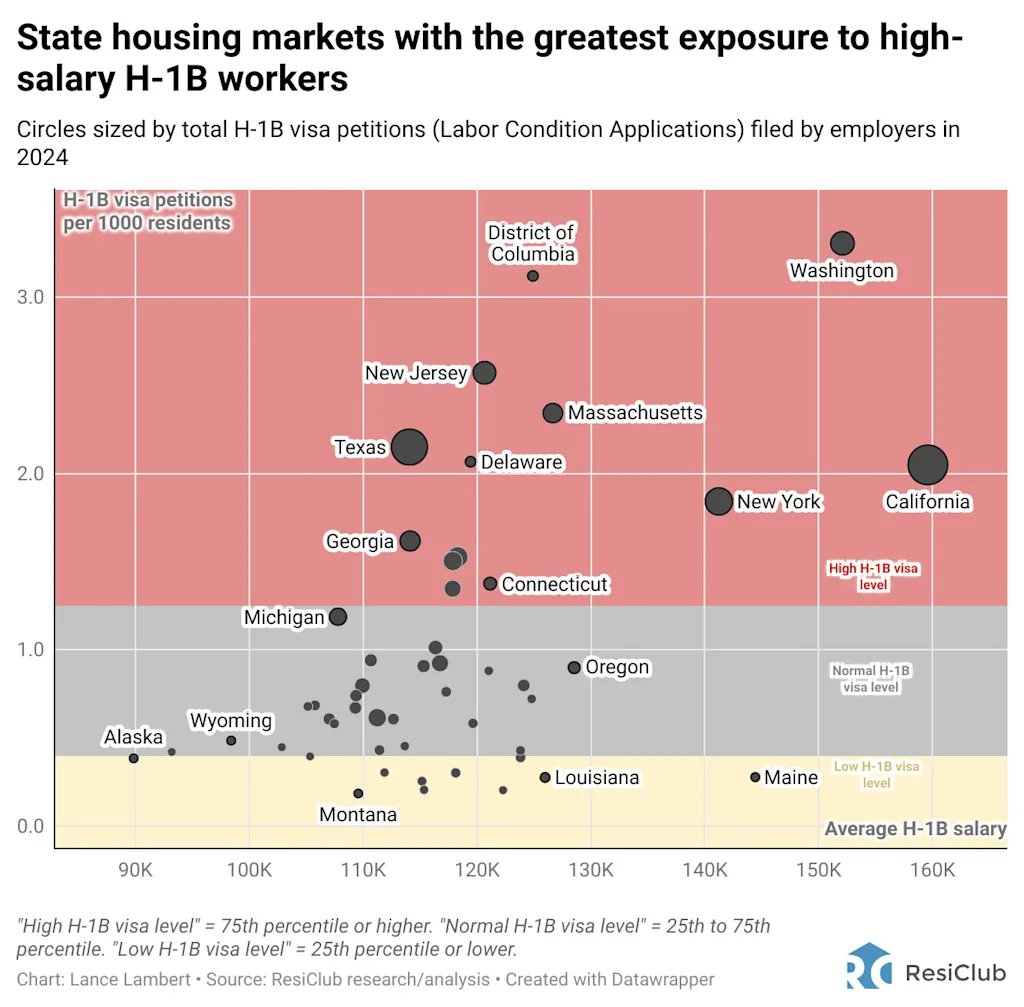

To run an apples-to-apples comparison that accounts for market size, ResiClub calculated H-1B visa petitions per 1,000 residents.

The states with the highest exposure to high-salary H-1B workers—and the housing and rental demand they generate—include Washington, California, New York, New Jersey, Texas, and the District of Columbia.

Click here for an interactive of the chart below

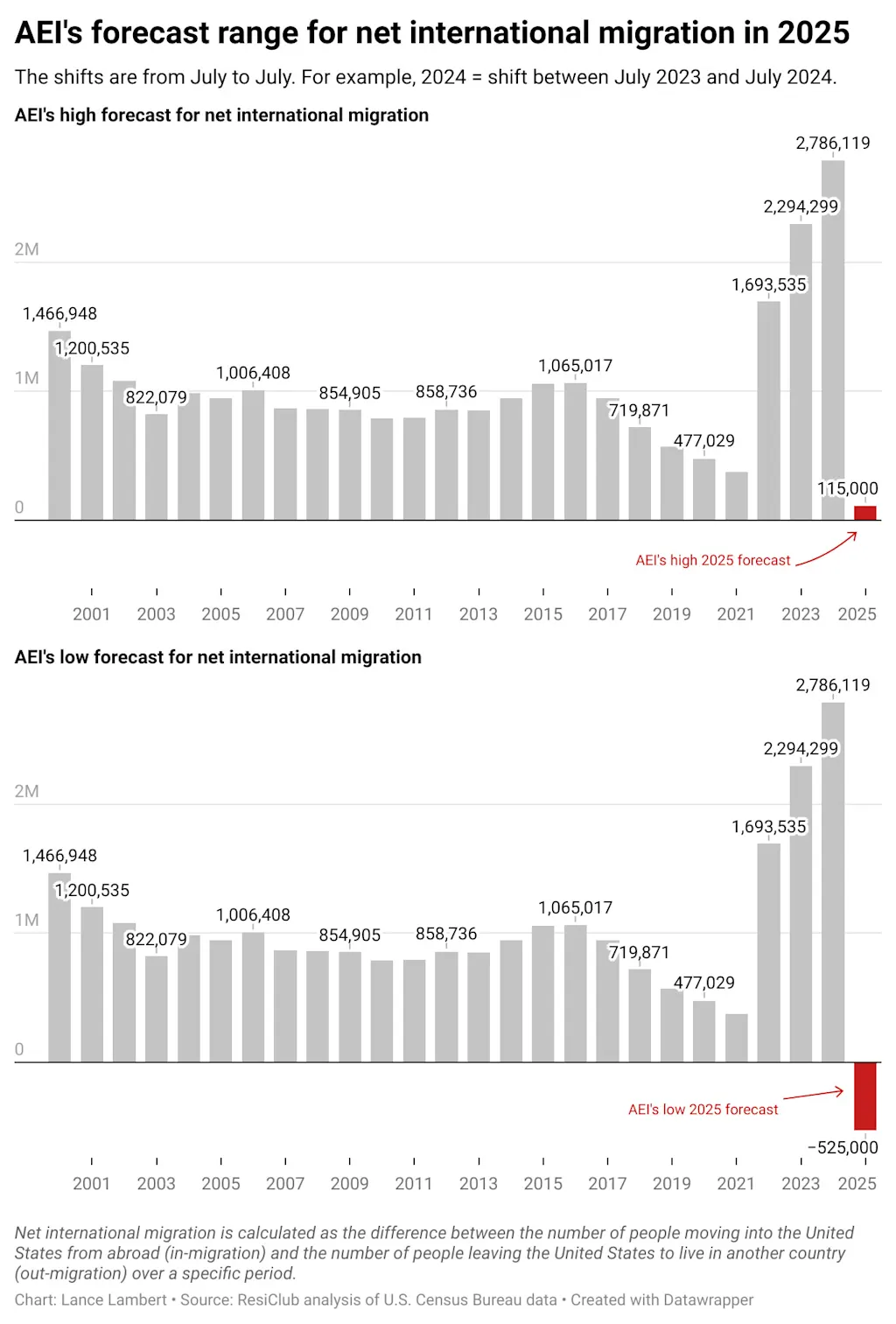

Zooming out to the big picture, we are in something of an international migration bust following a boom in 2021-2024.

Between summer 2021 and summer 2024, the U.S. saw a substantial upswing in net international migration—much of it coming through the Southern Border. As of July 2024, the U.S. population stood at 340.1 million, up 3.3 million from 336.8 million in July 2023. Of that population increase, 2.8 million (or 85%) came from net international migration.

That international migration burst, of course, is behind us now. Recently, border crossings have plummeted. A July forecast by researchers at AEI expects that net international migration in 2025 will be somewhere between +115,000 and -525,000.

What does this international migration slump mean for the U.S. housing market?

All else being equal, an immediate and direct housing impact of fewer immigrants coming through the Southern Border, in my view, is lower aggregate rental demand—specifically at the lower end of the market—than if that burst had continued. Rental markets likely to see the biggest impact are in metro areas that have experienced the most international immigration in recent years. In particular, major markets such as New York City, Miami, Dallas, and Houston could feel the greatest effects.