Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

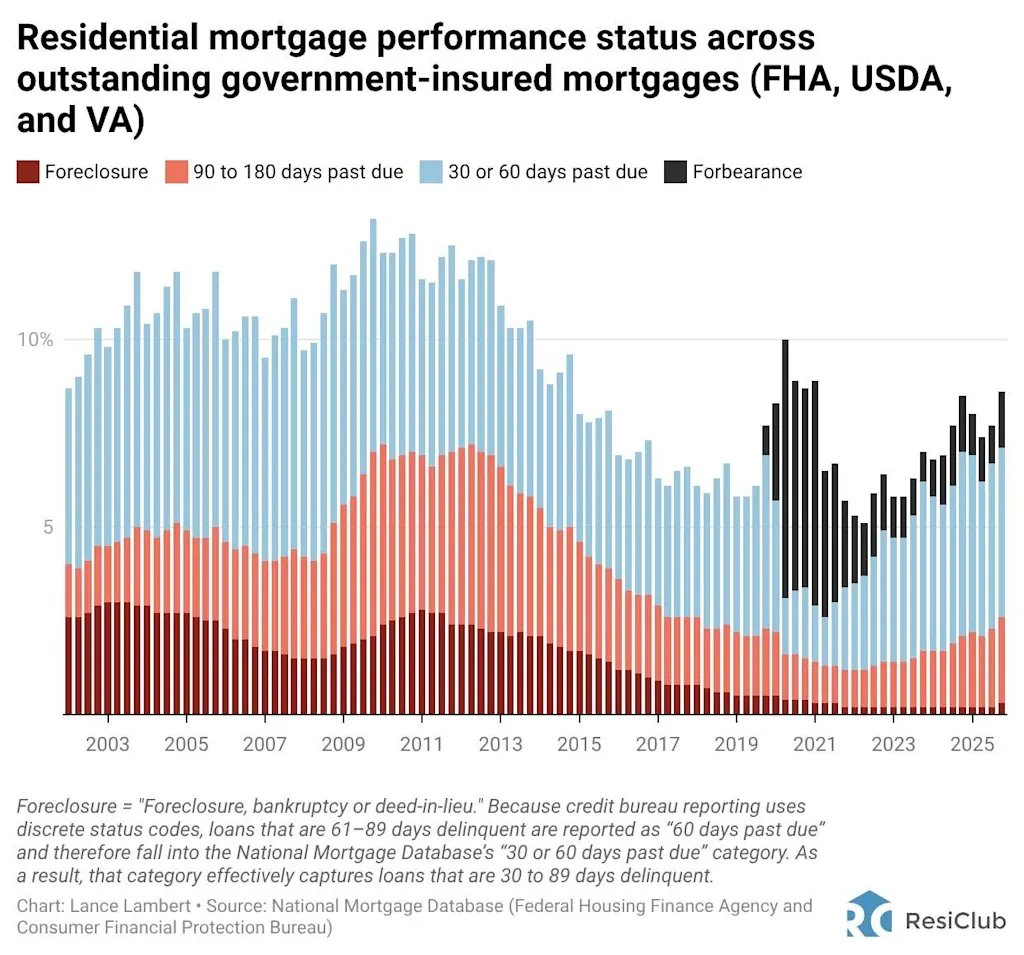

Before a home falls into foreclosure, the warning signs typically appear months earlier. A borrower first misses a payment or two, landing in the 30- or 60-day delinquency bucket. If financial stress persists, they fall further behind—90 to 180 days past due—and only around then (lenders generally can’t start foreclosure until a borrower is at least 120 days delinquent) does the foreclosure process typically begin.

This progression matters because the pipeline of early-stage delinquencies today tells us a great deal about where foreclosure activity is headed tomorrow.

Right now, that pipeline is small by historical standards—but it’s growing. Looking at the National Mortgage Database, early-stage delinquencies (30 or 60 days past due) have been ticking upward since 2022, and more serious delinquencies (90 to 180 days past due) have followed in kind.

The pattern is consistent with a housing market slowly normalizing after years of extraordinary intervention. When COVID-19 lockdowns began, the federal government implemented a nationwide foreclosure moratorium to protect homeowners from the economic fallout. These protections—including forbearance programs—were extended multiple times.

At the same time, a historic surge in housing demand pushed home prices to new highs during the Pandemic Housing Boom, boosting homeowner equity and keeping foreclosure activity unusually low. The data shows this clearly: foreclosure and serious delinquency rates cratered to historic lows around 2021.

But in recent quarters, foreclosures have steadily returned, inching closer to pre-pandemic 2019 levels. That foreclosure rebound picked up pace in Q1 2025, following the expiration of the moratorium on VA-backed mortgages. As those protections have wound down, the underlying stress that had been deferred—not eliminated—is finally surfacing in the data.

Still, perspective is critical. Current levels of mortgage distress remain a fraction of what the country experienced during the 2008 housing bust and the Great Financial Crisis, when total distressed mortgages—the share either facing foreclosure, 90 to 180 days past due, 30 or 60 days past due, or in forbearance—were 6.3% in Q4 2007 and peaked at 11.5% in Q4 2009, according to ResiClub analysis. Today’s comparable figure is roughly 2.9%—elevated relative to the pandemic housing boom’s historic low (1.4%), but nowhere near a systemic crisis.

While aggregate U.S. housing distress still isn’t that high, there are some pockets of concern with the government mortgage programs (FHA, USDA, and VA).

FHA mortgages—which are backed by the Federal Housing Administration and often used by first-time or lower-income homebuyers—have seen a notable spike in delinquencies over the past two years. Keep in mind that FHA mortgages make up a much smaller share of overall borrowers than, say, GSE conventional borrowers (guaranteed by Fannie Mae/Freddie Mac). According to the National Mortgage Database, as of Q4 2025, government-insured mortgages (FHA, USDA, and VA) represent 23.3% of the nation’s outstanding mortgage debt.

How does total housing distress—the share of all outstanding mortgages either facing foreclosure, 90 to 180 days past due, 30 or 60 days past due, or in forbearance—vary across the country right now?

Right now, the greatest concentration isn’t in the biggest boomtowns during the Pandemic Housing Boom—markets like Cape Coral and Austin, which have been undergoing post-boom ‘material’ corrections. Instead, the largest concentration of housing distress is in Louisiana and Mississippi, both of which have been hit by significant insurance shocks and consumer credit stress. Many pockets of Louisiana and Mississippi have experienced pricing weakness over the past few years despite not having run up that much beforehand, relative to other Sun Belt markets.

See state-level housing distress in Q4 2025 below.

window.addEventListener(“message”,function(a){if(void 0!==a.data[“datawrapper-height”]){var e=document.querySelectorAll(“iframe”);for(var t in a.data[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.source){var d=a.data[“datawrapper-height”][t]+”px”;r.style.height=d}}});

How does housing distress over the past several months compare to, say, during the early innings of the 2007-2011 housing downturn?

See state-level housing distress in Q4 2007 below.

window.addEventListener(“message”,function(a){if(void 0!==a.data[“datawrapper-height”]){var e=document.querySelectorAll(“iframe”);for(var t in a.data[“datawrapper-height”])for(var r,i=0;r=e[i];i++)if(r.contentWindow===a.source){var d=a.data[“datawrapper-height”][t]+”px”;r.style.height=d}}});

Total housing distress across most U.S. markets in Q4 2025 remains a fraction of what it was in Q4 2007, before the full weight of the Great Financial Crisis had even taken hold.

The biggest exception is Louisiana.