Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

On Wednesday, President Donald Trump announced: “I am immediately taking steps to ban large institutional investors from buying more single-family homes, and I will be calling on Congress to codify it.”

Soon afterward, Sen. Bernie Moreno (R-OH) tweeted that he’ll “introduce legislation in the Senate to codify this [ban] into law.”

The general idea has some support on the other side of the aisle as well. Back in February 2025, the Humans Over Private Equity for Homeownership Act was introduced by Sen. Jeff Merkley (D-OR) and cosponsored by Sens. Angus King (I-ME), Chris Van Hollen (D-MD), Ruben Gallego (D-AZ), Bernie Sanders (I-VT), and Mark Kelly (D-AZ).

Trump’s announcement on Wednesday raises a lot of questions that have yet to be answered. Is this just midterm-year politicking, or a policy proposal that could actually be enacted? Would such a ban be challenged in court? What qualifies as a “large institutional investor” under Trump’s proposed ban? Would it target only scatter-site acquisitions, or also build-to-rent developments? Would the ban require institutional investors to sell off their current single-family rental portfolios?

Given what we know today, I’ve outlined five things housing stakeholders should keep in mind.

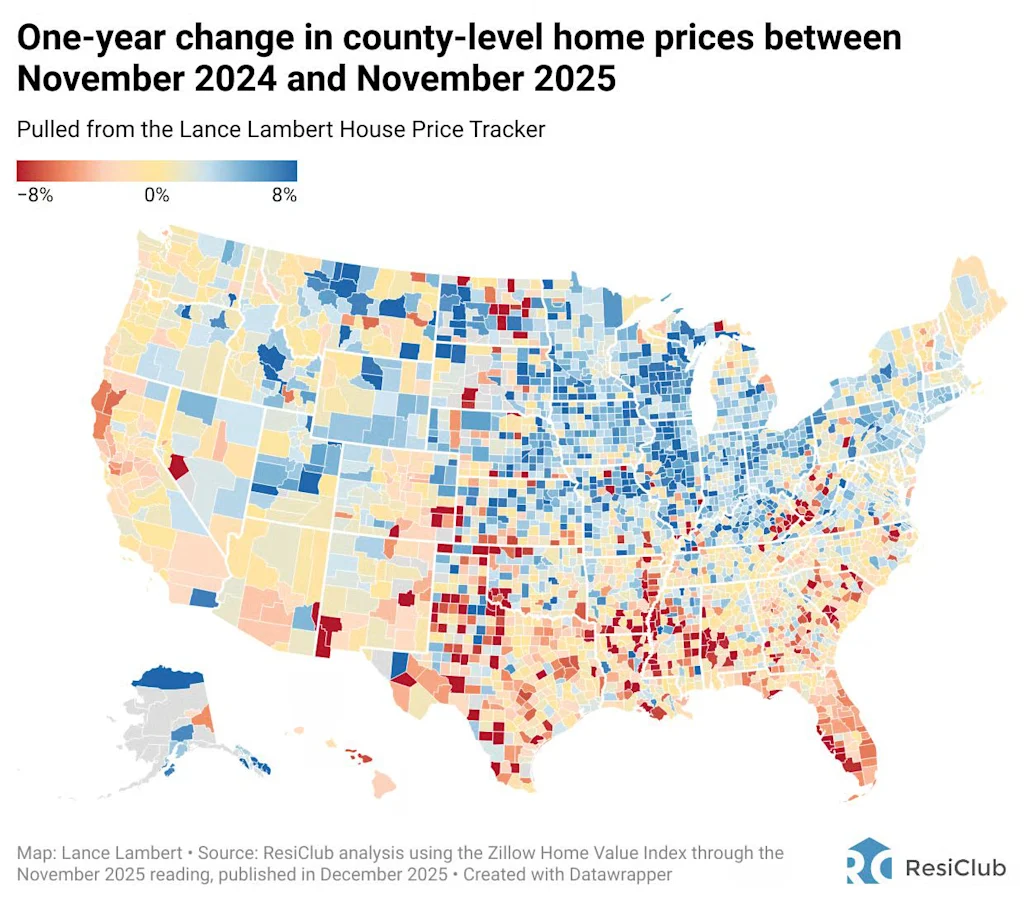

1. The effects of an institutional single-family home-buying ban would vary sharply by region

On a national level, “large investors”—those owning at least 100 single-family homes—only own around 1% of total single-family housing stock. That said, in a handful of regional housing markets, institutional and large single-family landlords have a much larger presence.

Markets like Phoenix and Atlanta became major hubs for institutional single-family rental (SFR) investment following the 2008 housing crash as the asset class started to institutionalize. Firms such as Invitation Homes, Progress Residential, and AMH built sizable portfolios in these metros by acquiring distressed homes.

That early activity helped establish a reliable local SFR ecosystem—including property management firms, leasing infrastructure, and contractor networks—that makes it easier to scale and expand single-family rental and build-to-rent operations today.

Following the bottom-buying wave, institutional capital remained concentrated in high–population-growth Sun Belt markets, where investors anticipated stronger long-term growth in incomes and overall rental growth.

Looking ahead, if a ban on institutional home-buying were enacted, its effects would likely be most pronounced in high-growth Sun Belt markets—especially in specific neighborhoods within metros such as Atlanta, Austin, Charlotte, Dallas, Jacksonville, Phoenix, and Tampa—where institutional ownership is more concentrated.

2. A forced institutional sell-off could temporarily put additional downward pressure on home prices in certain Sun Belt neighborhoods that are already experiencing corrections

Many of the Sun Belt markets with the largest institutional footprints are also among those already seeing home-price corrections. If a ban were to force institutions to sell existing holdings, some of these communities in places like Atlanta and Tampa could experience a short-term spike in listings from institutional sell-offs, adding further downward pressure in certain neighborhoods that already have downward home-pricing pressure.

But in Trump’s post, he said he wants to “ban large institutional investors from buying more single-family homes.”

That word, “more,” could imply that the proposal would not include a forced institutional sell-off, making the scenario above less likely.

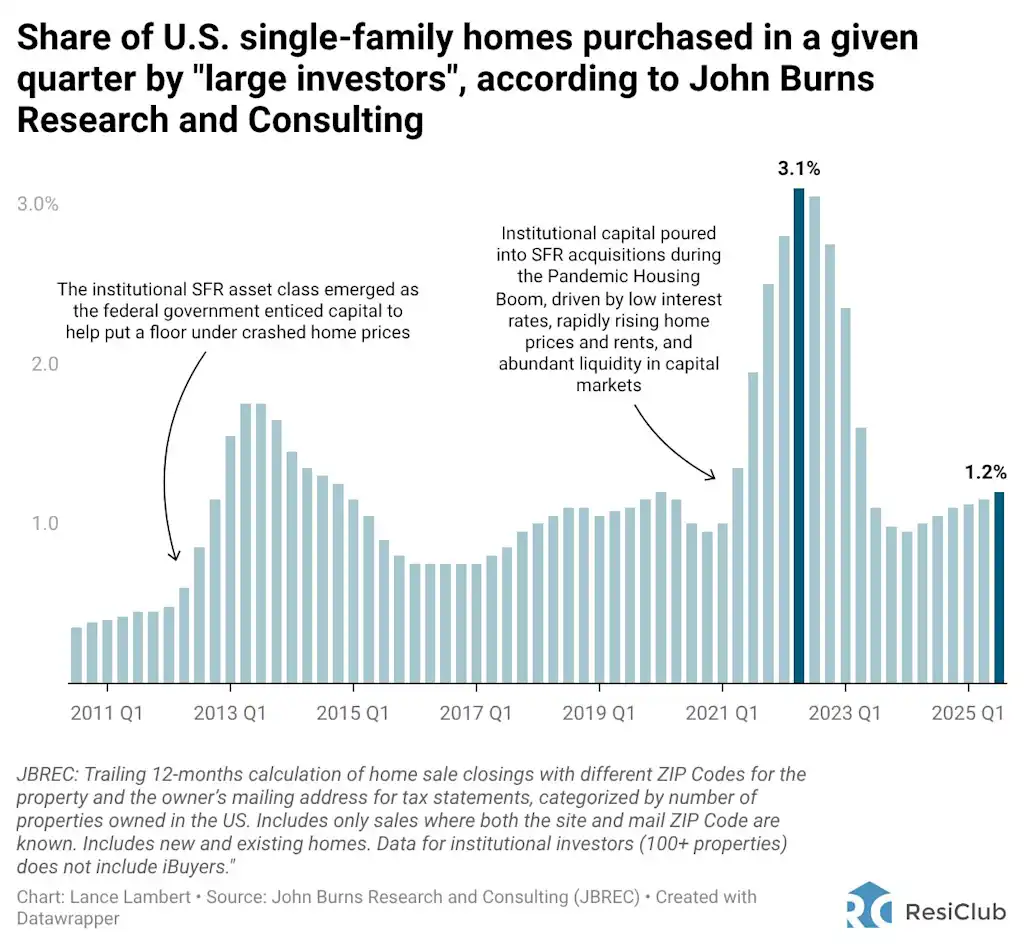

3. With institutional buying already well below Pandemic Housing Boom levels, there’s less demand left that can be squeezed out

If Congress were to ban institutional home-buying—and if the policy were to withstand legal challenges—it would reduce housing demand that currently accounts for about 1% of total U.S. home-buying activity. That contraction would have been much larger if the ban had been enacted a few years ago.

At the height of the pandemic housing boom, large investors—those owning at least 100 single-family homes—made up an all-time high of 3.1% of home purchases in Q2 2022, according to John Burns Research and Consulting. That period, at the tail end of the boom, was when yields were particularly attractive as borrowing costs were ultra-low, home prices were soaring, and rents were climbing rapidly.

However, since mortgage rates spiked and capital markets shifted, their share has fallen to around 1% of transactions over the past three years. The math isn’t as favorable right now.

4. A full-blown institutional ban—including a build-to-rent ban—could negatively impact U.S. homebuilding

One of the biggest questions right now is whether Trump’s proposed institutional ban would apply only to institutional scatter-site purchases (i.e., buying existing homes on the market) or also to build-to-rent development (i.e., building communities and homes specifically for rent).

If policymakers were to also restrict institutional build-to-rent development, it could have a noticeable negative impact on overall homebuilding later in the decade, in 2027, 2028, and 2029.

While single-family build-to-rent is currently only hovering around 8% of total U.S. single-family housing starts, it has driven much of the marginal increase in U.S. single-family housing starts in recent years. Back in pre-pandemic 2017 to 2019, single-family build-to-rent starts made up just around 3% of total U.S. single-family housing starts.

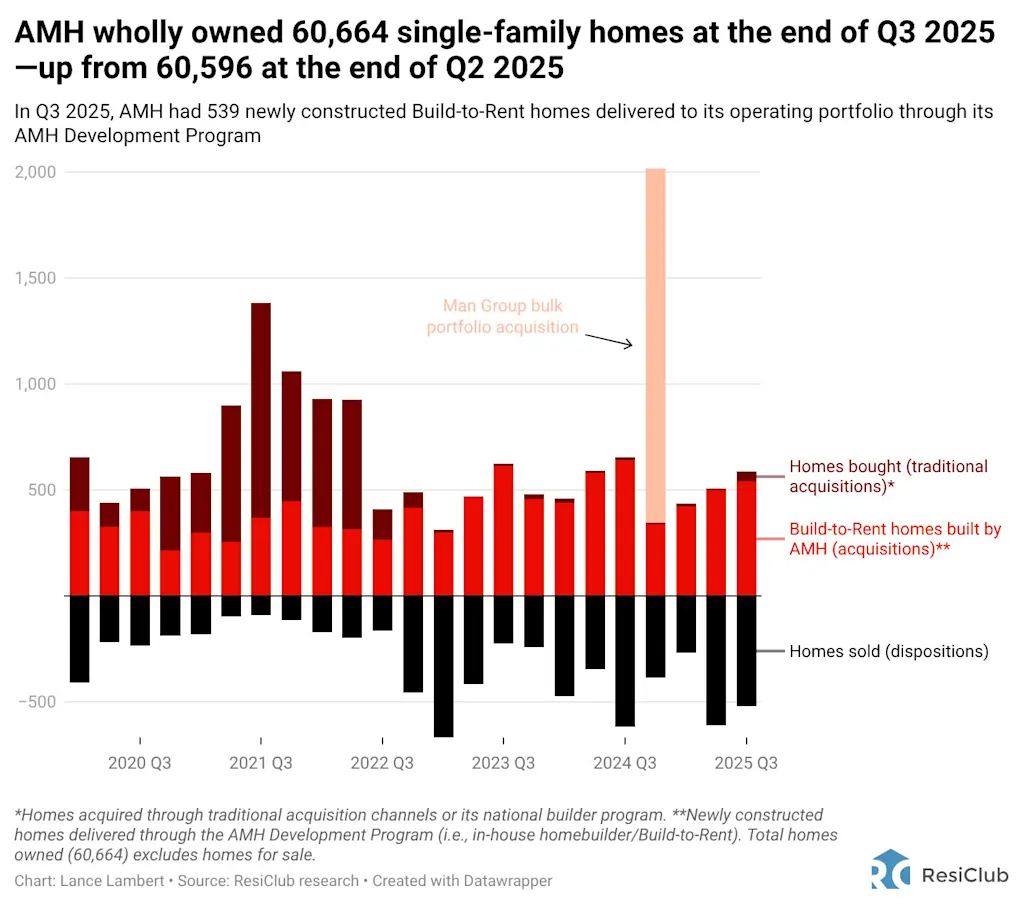

Look no further than giant SFR landlord AMH.

Not long after interest rates spiked in mid-2022 and the pandemic housing boom fizzled out, many institutional landlords, including AMH, stopped buying via the multiple listing service (MLS). However, AMH continued to barrel ahead, building its own single-family rentals.

Indeed, 95.7% of institutional landlord AMH’s single-family acquisitions through the first three quarters of 2025 came via its in-house homebuilding unit. According to Builder magazine’s Builder 100 list, AMH’s in-house homebuilding unit ranks as the nation’s 37th-largest homebuilder.

Housing analyst Kevin Erdmann, author of the Erdmann Housing Tracker, tells ResiClub that he believes banning institutional home-buying and build-to-rent would negatively impact homebuilding and, in turn, long-term housing affordability.

“American builders have been completing about 1 million new single-family homes annually since 2020—about 3 new homes per 1,000 Americans. That is a significant rise from the low of 1.4 new homes per 1,000 residents in 2011. It is roughly equal to the number of new single-family homes that were completed at the bottom of the 1982 recession. And, it is just over half the rate of homes that were typically built throughout the 20th century. Our problem isn’t that there are too many buyers for new homes. Our problem is that we are building too few. The main reason single-family housing construction has been so low is that the federal mortgage agencies that the Trump administration is in complete control of greatly limited access to mortgages after 2008. So there aren’t enough buyers. For decades, before 2008, big Wall Street firms weren’t involved in single-family housing at all because families that can get mortgage funding happily pay more for new single-family homes to live in than Wall Street will pay to rent to them out. The Trump administration could solve that problem by restoring late 20th century underwriting standards at Fannie Mae, Freddie Mac, and the FHA. But, instead, they apparently will add even more obstructions to the marketplace so that builders have nobody to sell new homes to while the rents American families have to pay to stay in the lousy supply of homes that we have skyrockets.”

5. Most institutionally owned homes are currently occupied—and most of their tenants can’t afford to buy right now

SFR landlords note that if Congress were to force institutions to sell off their housing stock, it could potentially displace thousands of current tenants who would need to find somewhere else to live.

Would those tenants turn around and buy?

Even in normal times, many single-family renters—whether their landlord is an institution or a mom-and-pop owner—can’t afford to buy the home they’re living in. That’s even more true at this point in the housing cycle, as the gap between today’s mortgage payments (i.e., a home at today’s prices/rates) and market rents has widened.

Sean Dobson, CEO of Amherst—which owns around 43,000 single-family rentals—tells ResiClub that “85% of their current tenants would not qualify to buy the homes they live in today.”

According to Dobson:

“Blaming institutional ownership for housing unaffordability is inaccurate and gets both the problem and the solution wrong. America’s housing crisis stems from years of policy failure, not the families who rent or the capital that houses them. At Amherst, we serve more than 200,000 residents, nearly 85% of whom would not qualify to buy the homes they live in today. Putting institutional rental housing at risk threatens real families and is unacceptable. Through private, unsubsidized investment, institutional capital restores neglected housing and delivers real solutions at a time when much of the housing finance system no longer works. Our industry is not the cause of the housing crisis; it is part of the solution.”