Want more housing market stories from Lance Lambert’s ResiClub in your inbox? Subscribe to the ResiClub newsletter.

Speaking at ResiDay 2025 on Friday, FHFA Director Bill Pulte broke news, stating that Fannie Mae and Freddie Mac will remain in conservatorship—easing industry fears that an exit could put upward pressure on mortgage rates. Instead, he said the government plans to sell up to 5% of their shares back to the public. Pulte added, “I anticipate that the president will make a decision either this quarter or early next year as it relates to the IPO.”

Pulte wasn’t done breaking news. Amid strained housing affordability, President Donald Trump and Pulte announced on X.com on Saturday that they’re working on a 50-year mortgage option to help lower some homebuyers’ initial monthly payments.

For today’s piece, I’m going to run through 11-data backed thoughts on 50-year mortgages. Before we get into the article, we should note that we don’t know the finer details of the option nor if they’ll actually go through with it.

1. A 50-year mortgage would come with a higher interest rate

Lenders charge more for longer-term loans because they take on additional risk. The further out the repayment period stretches, the greater the uncertainty around inflation, interest rates, and credit risk. Historically, the 30-year fixed mortgage rate has averaged about 57 basis points higher than the 15-year rate. If a 50-year option were introduced at scale, borrowers could expect an even steeper premium—likely adding another fraction of a percentage point to the rate in exchange for lower monthly payments.

2. Logan Mohtashami estimates that a 50-year mortgage would carry a rate roughly 42 to 57 basis points higher than the 30-year

Logan Mohtashami, lead analyst at HousingWire, tells ResiClub that he estimates that a 50-year mortgage would carry an interest rate roughly 42 to 57 basis points higher than the standard 30-year fixed mortgage.

The average 30-year fixed mortgage rate, as tracked by Freddie Mac, came in at 6.22% last week. At that level, the average 50-year fixed mortgage rate would be somewhere between 6.64% to 6.79%, assuming Mohtashami’s additional premium is correct.

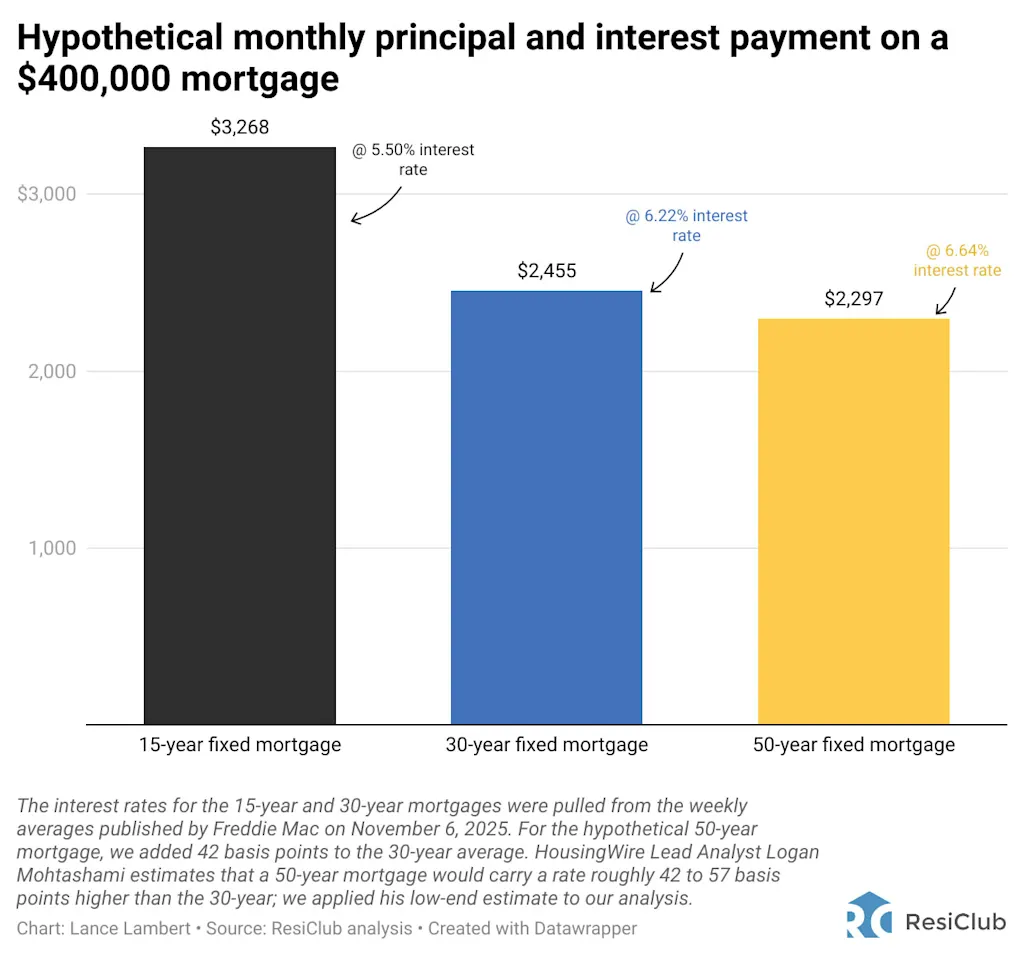

3. The monthly principal and interest on a 50-year mortgage would be a little less than on a 30-year

The core appeal of a 50-year loan is obvious: lower monthly payments. Stretching the repayment period over half a century spreads the same principal across 20 additional years, trimming the monthly cost. For example, on a $400,000 mortgage with a 6.22% interest rate, the monthly principal and interest payment would be roughly $2,455 on a 30-year mortgage. A 50-year mortgage at a 6.64% interest rate would lower that to around $2,297—a savings of about $158 per month, or roughly 7% less.

That could be meaningful for some homebuyers on the edge of affordability.

However, it’s far smaller than the monthly payment reduction that comes from moving from a 15-year mortgage to a 30-year mortgage.

Here’s what Logan Mohtashami, lead analyst of HousingWire, tells ResiClub:

“I truly empathize with the challenges that young homebuyers face as they embark on their journey to purchase their first home. They finance over 90% of their home purchases, and mortgage rates remain high compared to what they saw from 2011-2022. I applaud the administration’s efforts to support young homebuyers this year; their intentions are commendable.

Nevertheless, I worry that raising loan amortization will create other challenges. Higher levels of total interest payments and less equity buildup, all for just a few hundred dollars in savings—something a mere 0.50% to 1.00% decrease in mortgage rates could achieve instead from today’s levels It’s important to recognize that the housing market is already heavily subsidized through the 30-year fixed-rate loan and favorable tax policies.

As the market naturally shifts toward favoring buyers, we are seeing an increase in supply and a slowdown in [home] price growth. Historically, this is how the [housing] market has found its balance in other periods after big increases in prices such as we saw from 1943-1947 and 1974-1979—the aftermath of those periods didn’t have a housing bubble crash in prices, but in time affordability did get better.”

Housing analyst Aziz Sunderji, the founder of Home Economics, tells ResiClub: “My sense is that this is mostly policy theater. The fact is that prices and rates are high and there’s not much policy can do about that. Shifting from an already very long 30-year term to 50-year would be pretty marginal for monthlies and would of course do nothing to help lower down payments.”

4. A borrower would pay substantially more in total interest using a 50-year mortgage

The total interest paid over 50 years balloons. On that same $400,000 loan example, a 30-year borrower would pay roughly $483,000 in interest by the time it’s paid off. A 50-year borrower? Closer to $980,000—roughly half a million dollars more in financing cost. That gap is the trade-off between short-term affordability and long-term efficiency. The 50-year mortgage dramatically slows the pace of principal repayment, meaning homeowners stay “leveraged” for longer and build wealth through amortization much more slowly.

5. The vast majority of 50-year borrowers wouldn’t actually stick around for 50 years

A common online criticism of the 50-year mortgage is that it would leave borrowers paying well into retirement—or possibly never living to see the loan fully paid off. I’m not going to say that’s an invalid concern. But it’s important to keep in mind that most mortgages already don’t reach full term. Even with a standard 30-year fixed mortgage, few homeowners stay put long enough to make the final payment. The typical U.S. homeowner stays in their house for 11.8 years, according to Redfin.

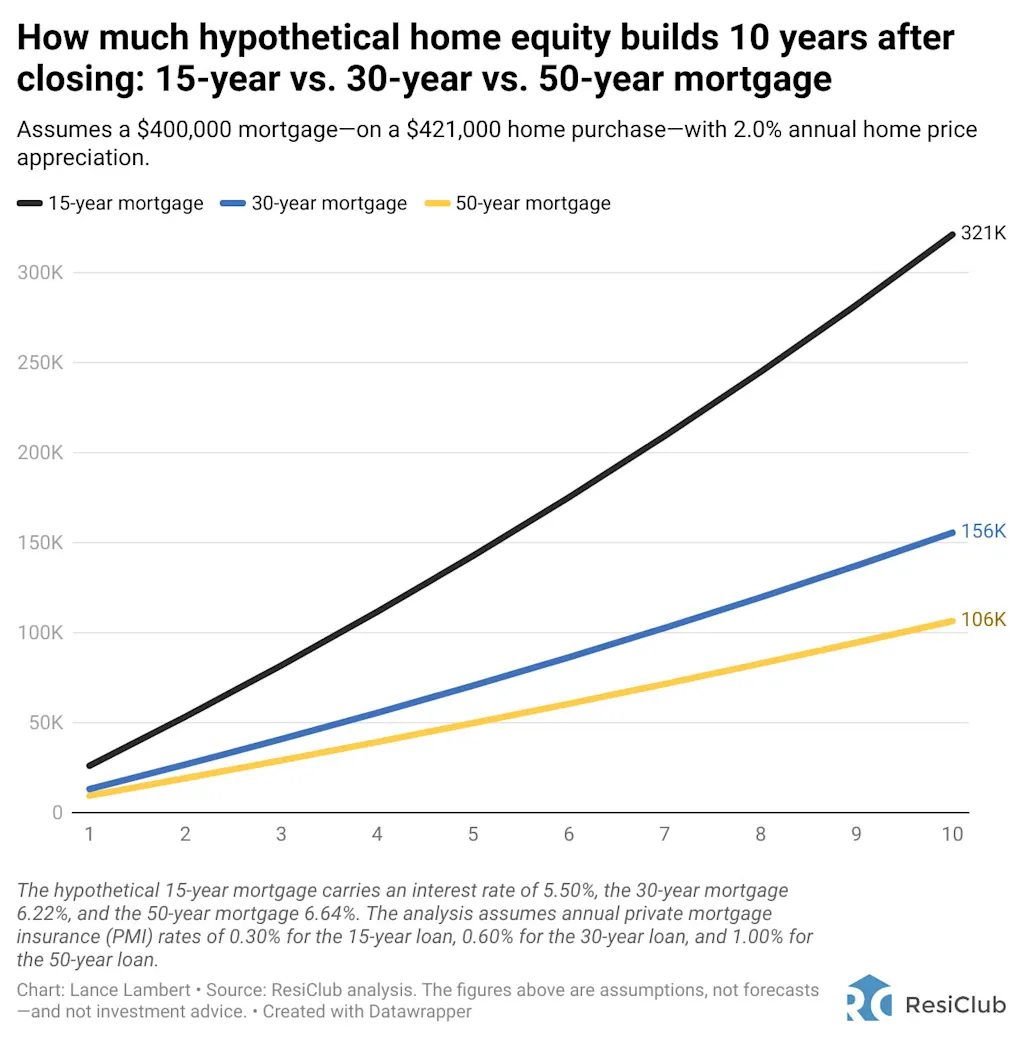

6. A 50-year mortgage borrower builds equity much slower

In the early years of any mortgage, most of the payment goes toward interest. Stretch that loan to 50 years, and it takes much longer before principal repayment meaningfully accelerates. In the hypothetical above, after 10 years, a 30-year borrower will have paid off roughly 20% of their balance. The 50-year borrower? Only about 9%. That means homeowners could feel stuck for longer—particularly if home prices flatten or dip. It could also make refinancing or selling in the early years trickier, since equity cushions take more time to form.

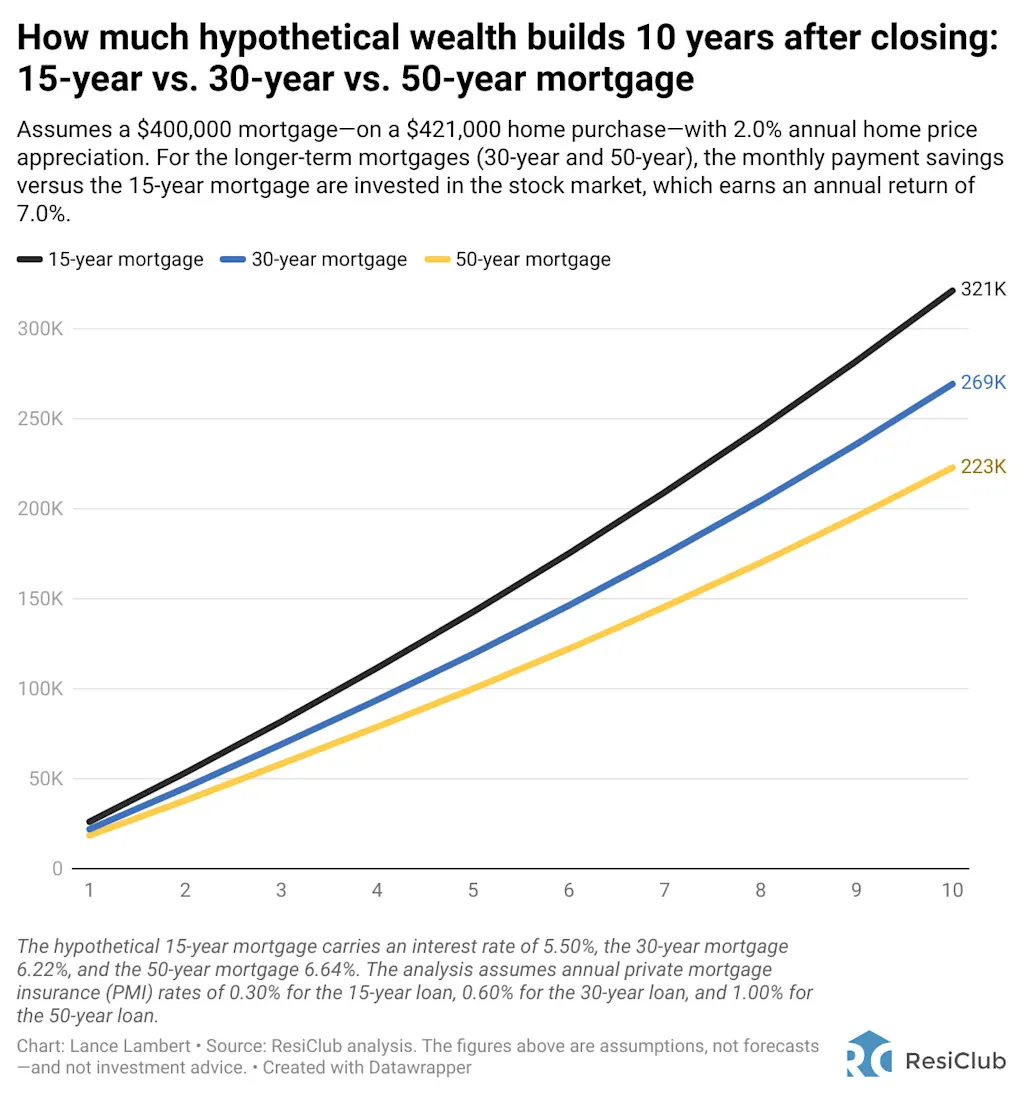

7. If the 50-year borrower invests their monthly payment savings, it makes up for some of the slower principal payoff

There is a counterargument: If 50-year borrowers invest their monthly payment savings (the difference between what they’d pay for a 15-year or 30-year mortgage), those returns could help offset the slower equity build. In a ResiClub analysis, assuming a $400,000 mortgage, 2% annual home price appreciation, and 7% annual investment returns, the 50-year borrower who invests their monthly savings does start to narrow the gap over time. The 15-year borrower builds wealth fastest through home equity, but over decades, the invested difference can partly close the wealth delta. Of course, that requires actually investing the savings.

8. In a weak home price appreciation market, a 50-year mortgage is less appealing

If home price growth remains modest for the rest of the decade while national affordability slowly improves, the 50-year mortgage becomes less appealing, according to ResiClub’s analysis. In a higher home price growth environment—like the 2012 to 2022 period—a 50-year loan becomes more compelling for borrowers whose choice is either buying with a 50-year mortgage (because they can’t afford a 15- or 30-year option) or continuing to rent and build no equity at all.

9. Rolling out a 50-year mortgage could create some additional housing demand—but it’s unlikely to be anything dramatic

A 50-year mortgage could pull a modest number of buyers off the sidelines. But don’t expect a huge housing demand surge. Given the math and housing backdrop (soft national levels of appreciation), the product would likely remain niche.

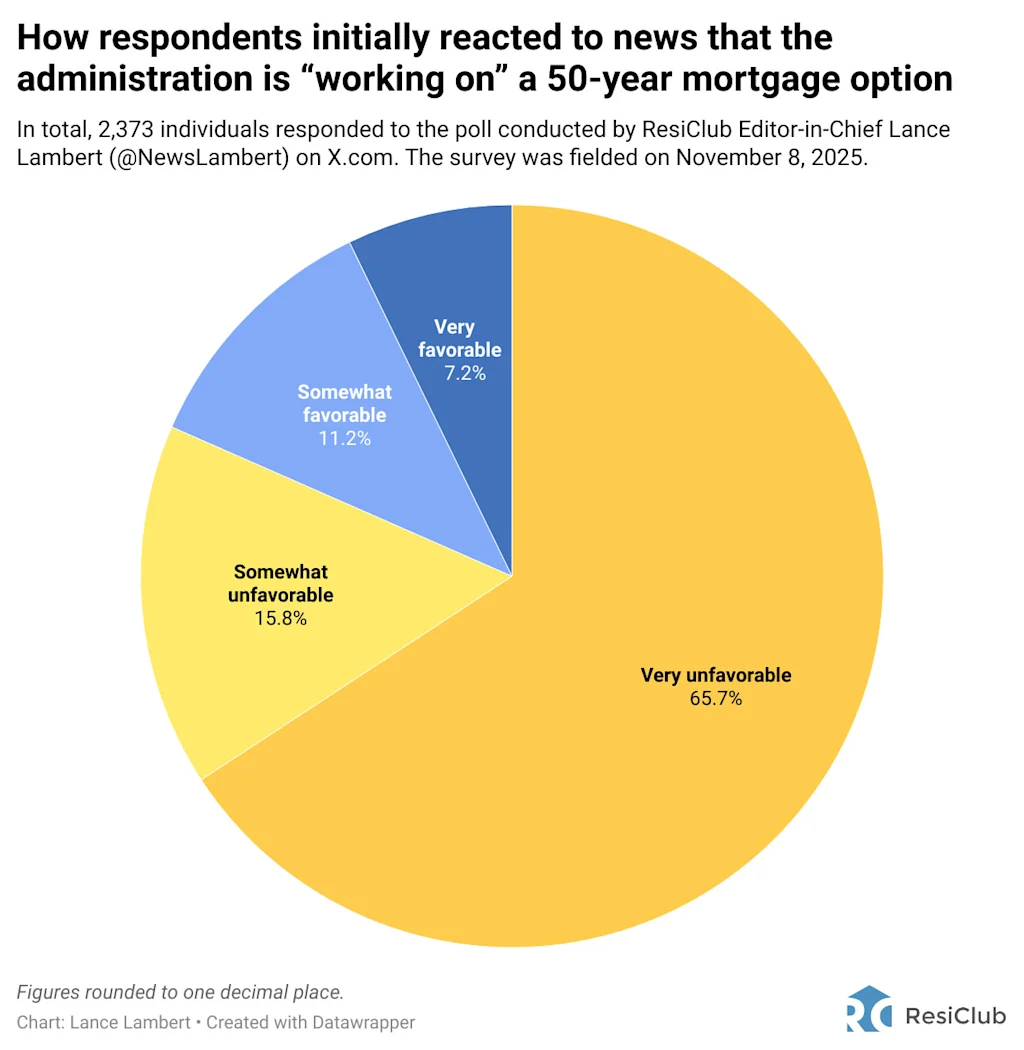

10. The public isn’t crazy about the idea

Early polling suggests the 50-year mortgage isn’t winning hearts. In a ResiClub poll conducted November 8, 2025, over 2,300 respondents on X.com weighed in on the Trump-Pulte announcement. A majority said their reaction was either “unfavorable” or “very unfavorable.”

11. The lackluster public response to the 50-year mortgage rollout decreases the likelihood of it happening

Without strong political or market enthusiasm, the odds of a true nationwide 50-year mortgage rolling out in the next few months remain low. For it to gain traction, it would require both regulatory approval and political will. The administration tested the waters—and given the response, it may stop short of fully implementing it.